Did RWE really abandon a long-planned offshore wind farm because of 'deep water'?

RWE is at pains to suggest that its withdrawal from the 1.2 GW, £4bn Atlantic Array was largely driven by unexpected technical difficulties. In the Financial Times, the company mentions the ‘deep water’ and ‘adverse seabed conditions’. We can be a little sceptical about whether this was the real reason: the company had been working on the Array since 2008 and submitted a full planning application almost five months ago. It seems implausible that a major European utility had devoted years of effort to the project only to find in late 2013 that the water was quite deep in the Bristol Channel.

We need to look behind the pretence and work out what might be actually happening. Perhaps when they said 'deep water' they had a metaphorical meaning in mind. I think RWE’s shift may be more to do with its increasingly perilous financial position and its recent change in corporate strategy. The Germany Energy Transition is marginalising RWE and the other large utilities as increasing levels of PV penetration devastate wholesale electricity prices. RWE is far less profitable than it was and is no longer able to raise the almost unlimited levels of capital necessary to finance the expensive shift away from fossil fuels. As a result, the company intends to make a transition from being the owner of capital-intensive power generation capacity and will move towards such activities as the provision of services for the ‘smart grid’. The consequences for the UK are serious: if the major German players (E.ON and RWE) in the UK electricity industry are unable or unwilling to finance investment in nuclear, wind or solar, who will do it?

RWE is at pains to suggest that its withdrawal from the 1.2 GW, £4bn Atlantic Array was largely driven by unexpected technical difficulties. In the Financial Times, the company mentions the ‘deep water’ and ‘adverse seabed conditions’. We can be a little sceptical about whether this was the real reason: the company had been working on the Array since 2008 and submitted a full planning application almost five months ago. It seems implausible that a major European utility had devoted years of effort to the project only to find in late 2013 that the water was quite deep in the Bristol Channel.

We need to look behind the pretence and work out what might be actually happening. Perhaps when they said 'deep water' they had a metaphorical meaning in mind. I think RWE’s shift may be more to do with its increasingly perilous financial position and its recent change in corporate strategy. The Germany Energy Transition is marginalising RWE and the other large utilities as increasing levels of PV penetration devastate wholesale electricity prices. RWE is far less profitable than it was and is no longer able to raise the almost unlimited levels of capital necessary to finance the expensive shift away from fossil fuels. As a result, the company intends to make a transition from being the owner of capital-intensive power generation capacity and will move towards such activities as the provision of services for the ‘smart grid’. The consequences for the UK are serious: if the major German players (E.ON and RWE) in the UK electricity industry are unable or unwilling to finance investment in nuclear, wind or solar, who will do it?

RWE’s problem

In the UK, we complain about the ‘excess profits’ of the large utilities. Investors in German power companies must utter a hollow laugh when they see these comments. RWE has just changed its guidance to the German stock market. Profits for the entire company, operating in several markets beyond its own national border, are projected to fall from €2.4bn in 2013 to about €1.4bn in 2014. Fossil fuel power generation returns are expected to decline to below zero by 2020. Partly as a result, Germany’s main business newspaper called it ‘a dinosaur on the brink’ yesterday.

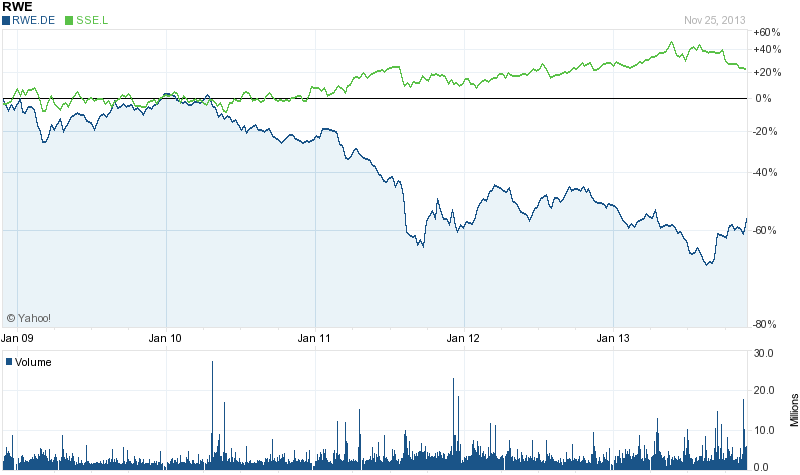

Contrast the experience of the UK’s SSE, the nearest local equivalent to RWE. Its share price (green line) is up 20% in the last five years compared to RWE’s 60% decline.

Share price chart

What’s driving RWE away from profitability? Germany’s energy transition away from fossil fuels has left the old companies with stranded assets. Some sources suggest that almost half the country’s fossil fuel plants no longer make any money. And why is this? The devasting effect on wholesale power prices of wind and solar power.

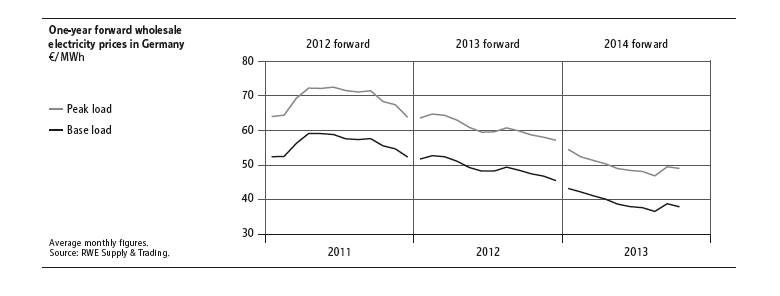

This can be summarised in one chart: RWE’s own figures for electricity prices in the forward markets. Chart 2 shows the graphs contained in the company’s summary of business conditions at the end of the third quarter. The wholesale price of electricity in 2014 has slipped to less than €40 a MWh, down from nearly €60 two years ago. Every megawatt hour RWE generates is worth a third less than it was. Few companies could hope to survive this price crash.

Chart 2

The UK Big 6 say rising wholesale costs mean that the retail price to UK households has to rise. In Germany, things are very different indeed. The market is now acutely vulnerable to the weather. Wholesale power prices fell to an average of less than €30 a MWh in the windy last week of October 2013 and dipped to below zero for several hours. This happens increasingly frequently.

Any large investor will look at Germany and assume that other countries will go through the same change. Subsidised renewables that produce power at zero marginal cost [1] increasingly dominate the local grids. Investing in electricity generation is becoming no job for cautious fund managers in Europe or anywhere else. Unsurprisingly, over 99% of new electricity capacity installed in the US in October was low-carbon.

Without profits from fossil generation, RWE doesn’t have the cash to invest in huge new wind farms off the Devon coast. Contrast the £4bn price tag for the Atlantic Array (which would generate about 1% of the UK’s electricity needs) with RWE’s expected worldwide profits of about €1.4bn next year. In addition to low cash flow, RWE also suffers from high financing costs. It complains that its investors demand much higher returns than are available on most renewable projects. Pension funds and insurance companies are better suited to investing in solar parks and wind farms. Not surprisingly, RWE itself has divested a substantial fraction of UK renewable capacity to special purposed vehicles set up to purchase existing wind farms.

RWE’s still secret but much discussed new strategy is a reaction to its problems of capital shortage and poor profits. A board document called RWE Corporate Story suggests that the company will move away from ownership of assets to what it calls a ‘capital-light’ approach. It will operate and maintain electricity generating plant but not own the expensive offshore wind turbines or anaerobic digestion plants that European countries are turning to. It will offer services such as supply/demand balancing to the operators of electricity distribution grids. Commentators have noted the resemblance to the evolution of the telecoms or mainframe computing industries twenty years ago. IBM used to be the world’s largest manufacturer of computers but it shifted rapidly into software and service businesses.

Other large utilities have suggested they will take a similar path. NRG, an important US power generator, openly forecasts that the electricity market will evolve rapidly towards more local and independently owner generation. Major utilities, whose business has changed less in the last fifty years than almost any other type of company, will be forced to switch strategy at an unprecedented rate, particularly in light of the falling costs of solar PV farms. David Crane, the CEO of NRG and an unusually frank commentator, says that US consumers are realising that ‘they don’t need the power industry at all’. Decentralised, small-scale wind and solar installations can supply all their needs when adequately backed up with storage or small gas-fired generators.

One final factor may have influenced RWE’s upsetting retreat from the Atlantic Array. In the company’s home country, offshore wind is becoming a nightmare for politicians. The transition to 100% renewables that Germany intends to make depends on putting a huge number of offshore turbines into the Baltic and North Sea. The country is waking up to the cost. A feed-in tariff of 19 Euro cents per kWh now looks increasingly unaffordable and the tortuous coalition negotiations between the two largest German parties are focusing on this number. Chancellor Merkel herself said that offshore wind subsidies needed to be concentrated on only the best offshore locations.

RWE must have felt that the same political debate is likely to happen in the UK where the proposed subsidy for offshore wind is also far higher than alternative low-carbon technologies. Indeed, a close reading of its press release this morning will demonstrate that it actually blames ‘market conditions’ as frequently as ‘deep water’ for its withdrawal from this vital project. (Readers from outside the UK may need to know that ‘market conditions’ in the energy market is a euphemism for ‘political commitment to high levels of subsidy’).

Here’s the problem in a nutshell: the UK and other countries need rich and large utilities to fund the energy transition (and I include nuclear, of course) but every step taken towards that goal tends to emasculate the power of the big existing players and reduce their ability to raise capital. As the dinosaur RWE advances towards the brink, who will step forward to put £4bn into a large wind farm? Many will respond by saying that we should switch instead to backing small scale and local energy production. Fine, I say: 3,000 of EWT’s excellent 500 kW onshore wind turbines would replace the power of the Atlantic Array. But where is the capital, the regulatory structure and political support necessary to get those windmills up within the next five years. I don’t see it yet.

(With many thanks to Gage Williams, who may not agree with my conclusions, for pointing me to the RWE and NRG documents).

[1] I apologise for the slightly technical language. The ‘marginal’ cost of something is the extra money a producer has to pay to create one extra unit of output. A gas-fired power station has to be pay for gas and wear and tear when it produces one more kilowatt hour of electricity. By contrast, an extra unit of power from a PV farm costs nothing.