'Grid Parity'

I gave a talk in Prof. Chris Llewellyn Smith’s course of lectures at Oxford University in late October. The SlideShare presentation is at the bottom of this article. This is the key chart from the lecture.

My primary purpose in the lecture was to suggest that assumptions about the relatively high cost of solar PV (and onshore wind and some other technologies) were based on errors. Correct these errors and PV gets to grid parity - usually assumed to be below £50/MWh or 5p per kWh- in the UK within a few years.

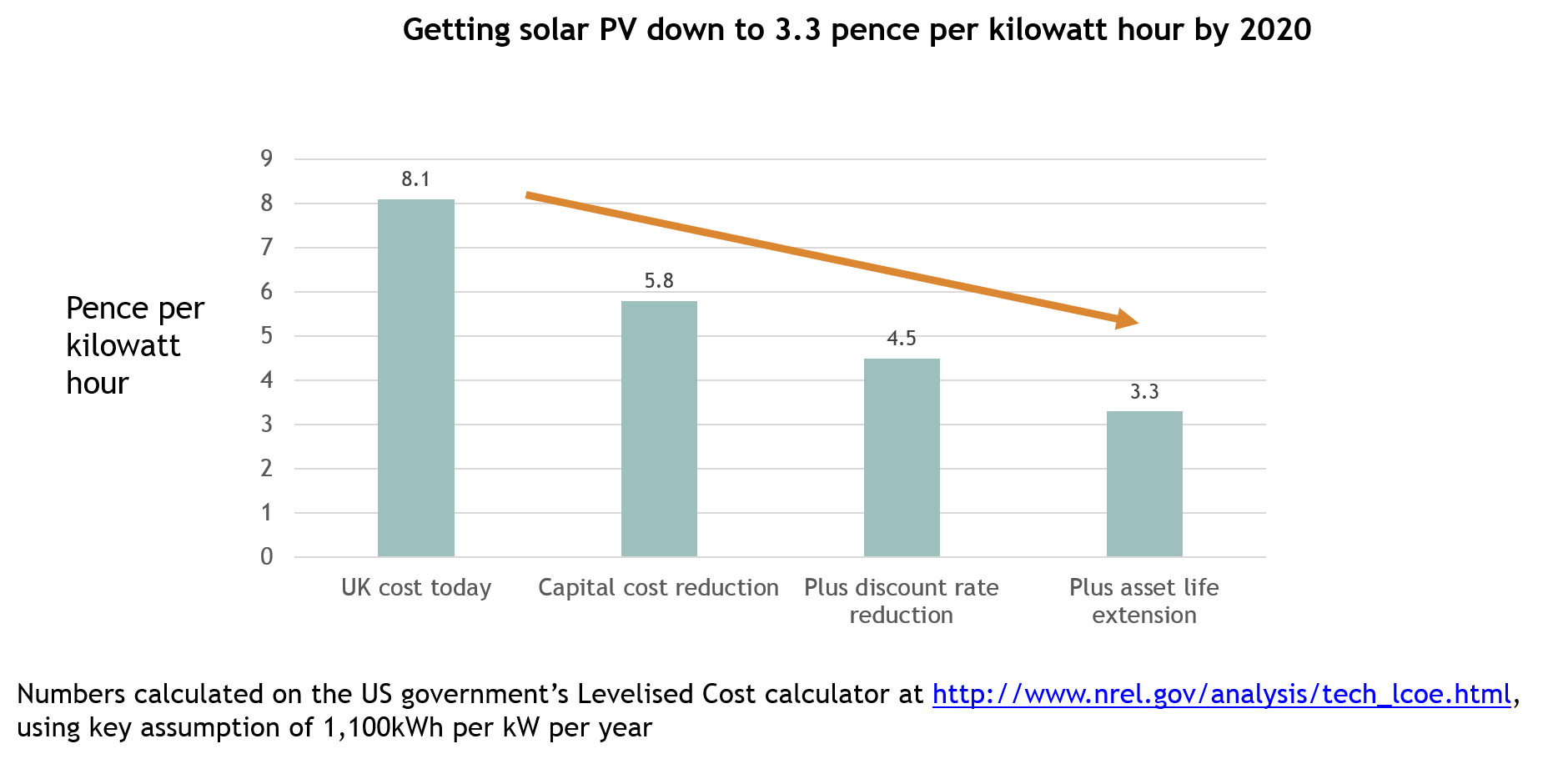

The chart merges the effects of three forces pushing solar PV costs lower.

1. UK policy makers are using almost ludicrously high figures for the cost of capital. And because solar PV is, in essence, a financial annuity, assumptions about the right rate are critical. A reduction from 7.5% to 2.5% in the real cost of capital will cut the levelised cost of electricity from PV by over a third. Is 2.5% a reasonable figure? I contend it is, based both on Fraunhofer’s figures for Germany and, second, on a small number of confidential transactions for which I have been given details. (These deals involved pension funds putting up 80% of the capital required for solar farms in the form of debt)

2. Second, PV panels probably have much longer lives than assumed. The evidence is mounting that we can reasonably assume that panels will last for more than 30 years. This is also vital to the economics of solar. Any asset that costs nothing to operate – which we can assume includes PV as a first approximation – will produce something much more cheaply if it lasts twice as long.

3. PV panels costs continue to fall in line with the predictions of a 20% 'experience curve'. Most manufactured item costs follow an experience curve that produces a reasonably predictable percentage decline for every doubling of accumulated production volume. The world has now produced about 200 gigawatts of PV panels. When we get to 400 accumulated gigawatts, costs will be 20% lower than today. And so on. Since even the dark-suited people at the International Energy Agency are now forecasting almost 5,000 GW of installed capacity in 2050, we can predict with some confidence that costs will fall to less than half the level of today. (1)

Taken together, I believe that today’s published ‘Levelised Costs of Electricity’ for PV are likely to fall to about 3.3 pence per kilowatt hour on the south coast of the UK by 2020. The most important driver is likely to be the reduction in the assumption about the required rate of return on capital. (And, please, may I politely say that I am often guilty of naïve optimism about progress in clean technologies but there is nothing in this forecast that assumes discontinuous change or particularly swift developments in manufacturing techniques. If we are able to coat silicon PV with perovskite semiconductors by 2020, progress will be even more rapid).

UK index linked government bonds (‘gilts’) are now trading on a yield of about MINUS 0.5%. (2) A solar farm with government guaranteed feed in tariffs, inflating by RPI, for the next 20 years is the nearest equivalent. The central point I tried to make is that any sensible analysis assumes that solar PV’s cost of capital has been dramatically pulled down in the wake of the unprecedentedly low interest rates in the world economy as desperate investors look for the safe yields provided by near zero operating cost capital assets such as PV farms or the Swansea tidal lagoon.

1. After the talk I was asked whether the ‘balance of plant’ costs can be expected to fall at the same rate as PV panels. I suggested that costs have been declining at an experience curve rate less than 20% but still very rapidly. I have been promised numbers to confirm this by a very large installer of UK panels with five years cost data and will update this article when the information arrive

2. This yield is calculated on the Retail Prices Index, which is currently running at 1.0% p.a. above the better designed Consumer Prices Index. So, at current rates, index gilts are offering about 0.5% real above CPI.